IRS Form 1099-C is an enlightening explanation that reports how much and insights regarding an obligation that was dropped. You can hope to get the structure from any bank that has excused an equilibrium you owe, expecting you to take responsibility for reimbursing it. You're expected to incorporate this dropped obligation as pay when you set up your government assessment form for the year the obligation was dropped.

What Is Form 1099-C?

A business stretches out cash to you when you get it, which could come as an advance dispensing or a charge card buy. Regardless, it would be best if you went into a consent to take care of that cash. It's not considered pay or dependent upon tax assessment since you won't keep it. The cash becomes paid and can be burdened when the loan specialist drops the arrangement expecting you to reimburse it. Structure 1099-C reports this pay and different insights about it, and you'll get a duplicate. The IRS gets it too, and the public authority anticipates that you should remember the pay for your expense return. IRS Form 1099-C Cancellation of DebtWho Uses Form 1099-C?

The IRS expects that organizations send Forms 1099-C to consumers when the bank drops or excuses more than $600 underwater. Organizations aren't expected to let you know the expense ramifications of dropping or excusing credits, yet they're committed to giving a 1099-C to you and to the IRS too. You'll utilize it to express the pay on your government form accurately, and the IRS will remember it for its record on you. A bank could drop your obligation for quite a few reasons, including:- The legal time limit for assortment has terminated.

- You've pursued a repayment consent to pay part of the obligation and have the other part dropped.

- The loan specialist has a business strategy of suspending assortment movement after a specific timeframe.

- You'll have no greater risk connected with that specific obligation after you've managed any duties.

How To Go About, If You Don't Receive Form 1099-C

Contact the bank if you realize you've had a credit dropped more than as far as possible; however, you haven't gotten a 1099-C. The oversight could be because of an administrative blunder, or maybe the loan specialist doesn't have your ongoing location. Try not to exclude the pay on your expense form just because you didn't get the structure. That can bring about punishments from the IRS. It's likewise conceivable that you will not get a 1099-C on the off chance that the advance isn't considered reportable to the IRS. There are certain circumstances in which it very well may be dropped, yet you don't need to report it as available pay: There would be no announcing necessity if the obligation were released in liquidation except if it was caused for business or speculation purposes. The IRS will neglect excused understudy loans through the finish of 2025. This change is important for the American Rescue Plan. Contracts on the main living place lost in dispossession or sold in a short deal or rebuilt contract fall into non-report status. You'll, in any case, have to remember this excused obligation for your expense form yet on IRS Form 982. Your state's duty regulation for dropped obligation could contrast with government charge regulation. Consult an expense proficient, like a bookkeeper or lawyer, to affirm your state's principles for detailing dropped accounts as available pay. You could get a Form 1099-A after a dispossession occasion or a Form 1099-C.Step-by-step instructions to Read and Use Form 1099-C

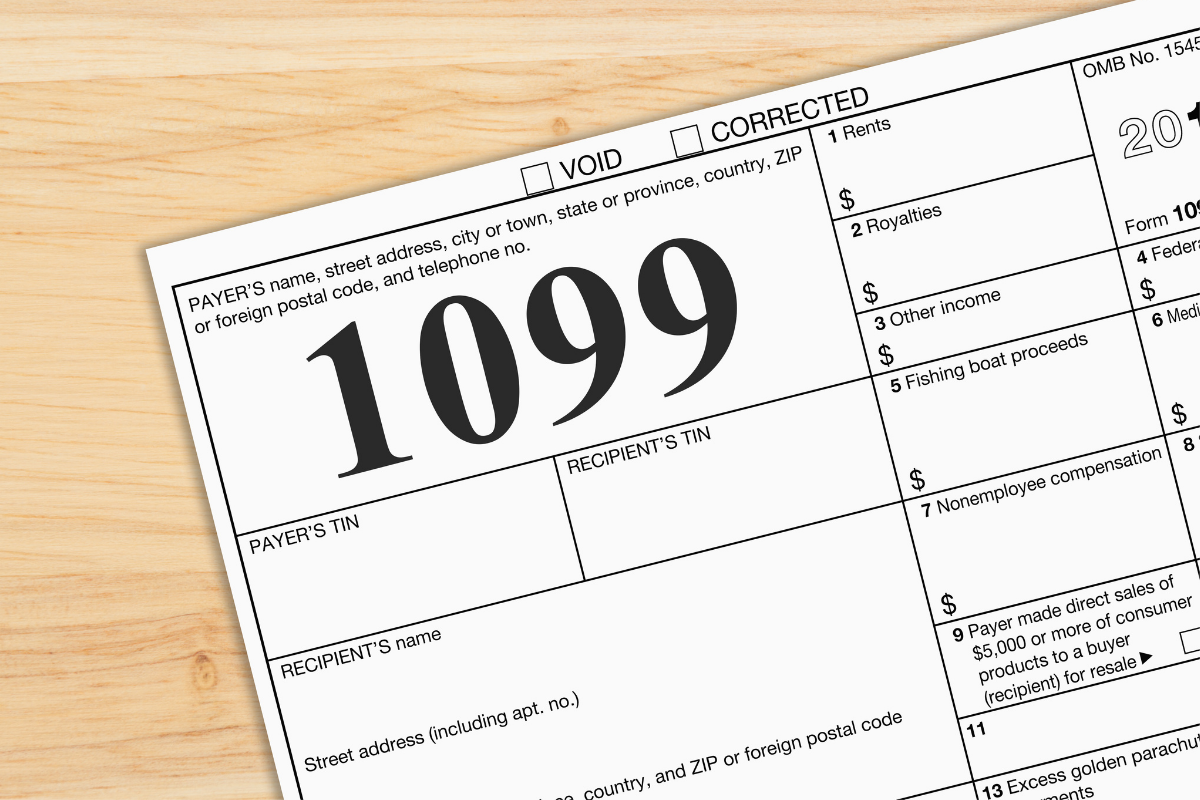

The name and distinguishing data for the loan boss who has pardoned your obligation will appear in the structure's upper left corner. That part additionally reports the bank's expense distinguishing proof number, your Social Security number, your name, your location, and the record number of your pardoned advance. The numbered boxes all relate to your debt:- Box 1 lets you know the date when the obligation was dropped.

- Box 2 refers to how much obligation was pardoned.

- Box 3 reports any interest that could have been remembered for the figure in Box 2.

- Enclose 4 depicts the obligation question.

- Box 5 states whether you were responsible for reimbursing the obligation.

- Box 6 is accommodated a code that distinguishes why the obligation was dropped.

- Box 7 would give the honest evaluation of any related property if the credit were a home loan, a vehicle credit, or for some other single-thing buy.

Necessities for Form 1099-C

You don't need to present the 1099-C with your government form when you record it because the IRS now has a duplicate. You ought to incorporate it with your other monetary archives when you go to your assessment preparer, be that as it may. Ensure your duty proficient has insight with this kind of pay. You don't maintain that this issue should catch up with you. Your assessment form may be dismissed, assuming you neglect to incorporate the pay. Alternatively, the IRS could address your return and change your discount or send you a bill for any extra sum that is expected, assuming you neglect to incorporate the pay. You could have to deal with fines and additional damages if the pay isn't accounted for and any related duty isn't paid on time. You could likewise need to converse with a duty proficient if you were bankrupt when the obligation was dropped because you probably won't need to report the payment. You were ruined if your total liabilities were more than the honest evaluation of all your resources at that point. You had total negative assets when the credit was dropped, so you can document IRS Form 982 to take a bankruptcy rejection for dropped debt.Key Takeaways

IRS Form 1099-C reports a dropped obligation to you and the IRS when a bank excuses an excellent credit you owe and no longer considers you liable for paying it. The IRS takes the place that dropped obligation is available to pay to you and should be accounted for on your government form. Moneylenders should give Form 1099-C when they excuse obligations of more than $600. A few obligations, for example, most obligations released in liquidation, aren't reportable on Form 1099-C.