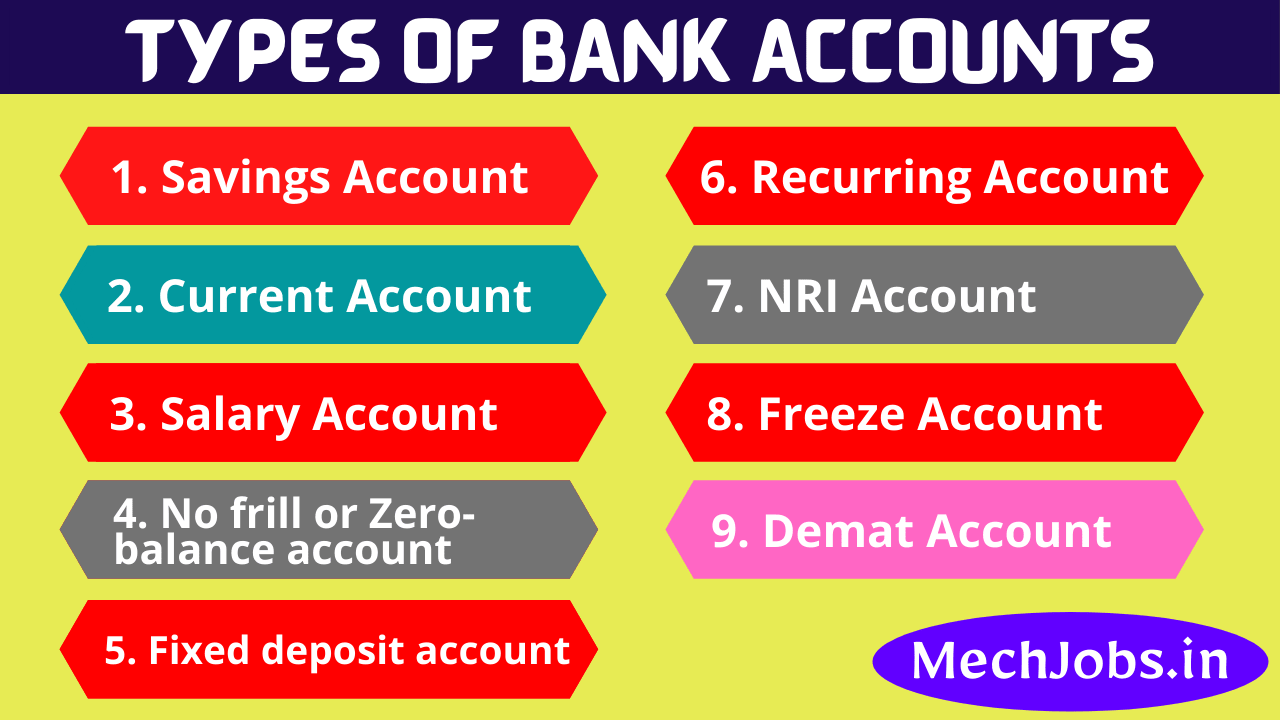

Saving your hard-earned dough is essential! However, keeping wads of money stuffed under your mattress probably isn't the proper thanks to set about it. We recommend storing your funds in a checking account instead. But what are the kinds of bank accounts you'll use? Approximately 95% of homes in the United States have a checking account. There are several different types of bank accounts out there, so it'd be hard to understand which one is true for you. Be it a standard checking account or a depository financial institution account. Let's re-evaluate the various checking account types so you'll decide which type to open. You'll even want to open multiple accounts once you get the hang of it!

Checking accounts

A bank account may be a must-have for anyone with bills, i.e., everyone. It allows you to form withdrawals within the sort of checks, debit cards, or transfers. There are not any limits on these withdrawals, making checking accounts perfect for paying your rent, MasterCard bill, and more. You'll have fast access to cash, which is great if you've got your paycheck deposited here. That said, there are a couple of drawbacks to the present sort of account. Usually, they don't offer interest or much in the least, which suggests you won't get anything for storing your money with them. Also, some may include maintenance fees monthly if you don't meet specific requirements. There also are usually overdraft fees if you pull extra money from your account then you currently have.What to see for

If you're within the marketplace for a bank account, confirm the one you discover doesn't have a required minimum balance. If your balance falls below a certain threshold, you don't want to be charged a fee. You'll also want an account that gives direct deposit and online banking. These features make it simple to keep track of your finances. Finally, though it's as rare as a unicorn, try to find a bank account that pays tremendous interest so you can make some extra money while your money sits idle.Savings accounts

Put cash in a bank account if you don't want to utilize it for bills but don't want to take a risk. It's an excellent place for your emergency fund because you'll still have access to money once you need it. And better of all, bank accounts typically earn interest! Interest is calculated to support your monthly balance and, therefore, the APY of the savings account. Unfortunately, bank account rates are often relatively low. As an example, at the time of this writing, the national average is sitting at 0.05%. If you've got a bank account with $1,000, you'll only earn $0.50 in interest for the whole year! Ugh. Another problem is that you can't make quite six transfers or withdrawals during a month employing a bank account. This is often a federal law, and if you break it, your account could also be closed.What to see for

While the national average rate of interest for savings accounts is low, that doesn't mean all interest rates are low. You'll find some rates closer to a quarter if you go searching. These are typically provided by online-only banks that do not have a physical location. Look for no-fee savings accounts. The majority of them don't have these, but when you register an account, make sure to read the fine print.Certificates of deposit (CDs)

If you're lucky enough to possess some money you don't get to touch for a short time, a CD could be an ethical choice. It offers you higher interest rates than a bank account. All you've got to try to do is choose a pre-defined term and keep your money within the account during that point. If you are doing that, you'll be rewarded with extra money than you started with. Standard terms include 12 months, three years, and five years. That said, the rate of interest for CDs also trends pretty low. The typical national rate for a 12-month CD but $100,000 is simply 0.15% as of this writing, which isn't far better than a bank account. If you would like to tug your money before the term is up, there is also a drag. You'll need to pay the penalty, which can effectively negate any earnings you had from the CD.What to see for

Consider CDs that provide flexible withdrawal options. For instance, some might allow you to withdraw early without paying the penalty fee. The con side of this is often that rates are usually lower. You'll also want to buy around and find CDs with the simplest interest rates. Confirm the speed is worthwhile to tie your money up for an extended period. Finally, consider CDs with flexible term options. For instance, if you recognize you'll need money to buy a replacement baby in about nine months, find a CD that will accommodate that timeline.Money market accounts

Let's get into other sorts of bank accounts! Wouldn't you like there was a hybrid of a checking and savings account? A market account is the closest you'll get thereto combo. It allows you to earn higher interest than a bank account on your money while still having the power to write down checks. And since there are not any penalties for withdrawals like with a CD, you'll access your money whenever you would like it. It's quite the favored option, as 10% of U.S. adults keep their savings in one. Just confine your mind; you'll pay a premium for the prospect to earn higher interest. Checking and savings accounts usually have lower minimum balances and fees than market accounts. Plus, the six-withdrawal limit still applies, so you'll get to take care of what percentage times you pull money monthly.What to see for

The significant advantage of a market account is earning higher interest, so confirm the account you select pays well lately, which may be tricky because the national average rate is simply 0.07% as of this writing. You should also carefully look over any and every fee the account will charge you. Find a credit card with minimal or no fees for things like maintaining a minimum balance, so you don't lose out on interest.Retirement accounts

Saving up, so you've got money to retire is crucial, and retirement accounts can assist you in getting there. These are accounts that are geared for long-term investment. In most cases, you'll leave the money in these accounts until you're in your 60s or 70s. Your two main options for retirement accounts are an IRA and 401k. An estimated 54% of individuals who aren't retired have a 401k or 403b, while 33% have an IRA. That said, 13% of individuals age 60 and older who aren't retired haven't any retirement savings! Yikes, don't let this be you.