Electronic payments that are processed through the Automated Clearing House (ACH) Network are referred to as ACH payments. With the assistance of a centralized system that guides the funds to their ultimate location, financial resources can be transferred from one bank account to another. These computerized payment methods can be advantageous for merchants as well as customers in the following ways: When payments are made electronically, they are less expensive, they can be automated, and the process of keeping records is frequently simplified. Even though you may not be familiar with the technical jargon, the majority of people have already begun using ACH payments. It is typically the responsibility of the ACH network to process payments such as direct deposits of wages by employers and electronic withdrawals of payments from checking accounts by customers of online bill pay services. According to Nacha, the Electronic Payments Association, which is the organization that oversees the ACH network, consumers and businesses made more than 23 billion ACH payments in 2018.

The Fundamentals of the ACH System

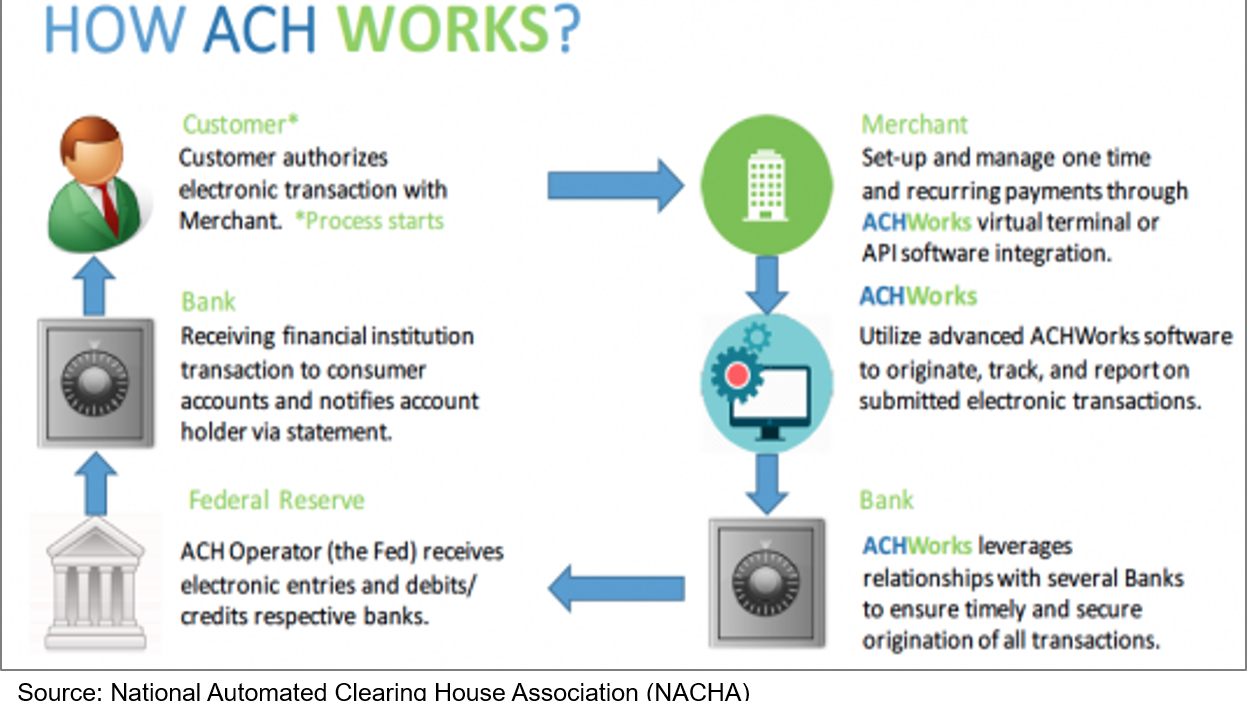

Electronic funds transfers from one bank account to another are what are known as ACH payments. Several examples include:- Payment is made to a service provider by a customer.

- When an employee is paid, the money is deposited into their personal checking account by their employer.

- An individual customer moves their money from one bank to another.

- A supplier receives payment from a business for the goods it sells.

- A taxpayer can electronically transmit funds to the Internal Revenue Service (IRS) or to local organizations.

- The name of the financial institution or credit union that will receive the funds.

- The kind of account that can be opened at that bank (checking or savings)

- It is the ABA routing number for the bank.

- The account number belonging to the recipient

Benefits All Around

There are many reasons for the widespread adoption of electronic payment methods. ACH payments require a lower amount of resources than conventional paper checks do because of their electronic nature. It is no longer necessary to use paper, ink, or fuel to transport checks, nor does it take as much time or require as much labor to process and deposit checks. The use of electronic transactions makes it simple to record one's earnings and expenditures. Banks generate an electronic record of every transaction that takes place. The transaction history can also be accessed by accounting software and personal financial management programs.The Advantages of ACH Transactions for Businesses

When businesses switch to accepting electronic payments, they can realize cost reductions and improvements in their operations.Simple to Work With

Businesses are required to wait for the check to arrive in the mail from customers who pay with checks, and then they must take the check to a bank to be deposited. The process of entering payments into a recordkeeping system can be laborious and can result in the occasional misplacement of payments. There is no need to send paper checks to the bank and wait a few days to find out which checks were returned as unpaid when using electronic payments because they arrive promptly and reliably.Comparatively Cheaper Than Plastic

Processing an ACH transfer typically results in lower fees for a company that also accepts payments made via credit card than does accept payments made via credit card. Especially when collecting a large number of payments on a recurring basis, those cost reductions add up. The benefits are only going to grow as a result of automating those payments. However, unlike a credit card terminal, an ACH terminal will not provide you with an immediate response of either approval or denial.Payments Made Over a Great Distance

Although it is also possible for businesses to accept credit card payments remotely, ACH payments can be accepted. ACH is an option that could solve the problem for your customers who either do not have credit cards or who would rather not provide their card information on a regular basis.The Advantages of ACH Payments for Customers

Customers aren't the only ones who can reap the benefits of ACH payments; businesses do too.Payments Made Easily

There is no longer a requirement for customers to write checks, reorder checks when they are depleted, or send checks in the mail by the appropriate deadline. They will not have any charges applied to their credit cards because the money will be taken directly from their bank account.Autopilot

Customers who pay with automatic ACH payments do not need to be concerned about keeping an eye out for bills or taking any action when it comes time to make payments. Everything is on autopilot, which can be both a blessing and a curse.How to Facilitate Customers' Automated Clearing House (ACH) Payments

You will need to work together with a payment processor if you want to accept payments through ACH. It's possible that you already have a working relationship with one of them; you just aren't utilizing their ACH service just yet. There are many payment processors that can assist you in accepting ACH payments; therefore, it is in your best interest to shop around for one that precisely meets your requirements. You should begin by inquiring with the companies that are already providing you services regarding the possibility of them enabling ACH payments for you. These companies include:- The financial institution in which you maintain your company's accounts.

- The business that already handles your payment processing for credit cards (or other types of payment)

- Your choice of accounting software; today's most popular packages give you the ability to generate invoices and take payments via ACH.

What is the price tag on that?

ACH is a method that can be utilized by companies of any size. If you have a higher volume of transactions, you will naturally pay less per transaction; however, the same logic applies to credit card payments. The fees associated with sending and receiving ACH payments are typically around $0.29 per transaction on average. 10 It's possible that service providers will have higher prices for small businesses. Others include a monthly fee, while still others take a percentage of each payment or charge a fee per transaction as their revenue model. It is possible that these costs are still less than the fees associated with processing debit card payments, depending on the average ticket size of your customers. When considering different options, it is important to keep the big picture in mind: Accepting checks might not incur any additional expenses, but what are the potential drawbacks of doing so? Working with paper checks is time-consuming, and it's likely that the funds won't be deposited as quickly as they would be otherwise. For some companies, such as consultants who only receive one or two checks per month and for whom cash flow is not a concern, setting up ACH may be more trouble than it is worth. This is especially true for businesses that do not accept credit cards as a form of payment. However, others may come out on top simply by increasing the amount of available time in the day. When you automate your payments, you free up resources that can be put toward other endeavors.Payments Made Via Personal ACH

If the party on the other end of the ACH transaction is a business or other organization, you, as an individual, will be able to send and receive payments through this system. It can be difficult to set up ACH payments between two individuals directly, but it is simple to transfer money when there is a third party involved.Apps from a Third Party

You can send money to family and friends completely free of charge thanks to a number of different apps and payment services. These apps provide a front-end to your bank account and frequently use ACH to make deposits and withdrawals on your behalf. They also provide access to your bank account.Bank Offerings

It's possible that your financial institution, like a bank or credit union, offers a P2P payment service that also lets you send money. These services may be marketed under the name of a specific bank, or they may be a component of Zelle or Popmoney. Unfortunately, a person cannot simply "punch in" the banking information of another person in order to complete a transfer of funds to that person. It is possible that the person you are sending money to or receiving money from will need to create an account with the service provider in order to complete the transaction. This will depend on the service that you use (or at least provide their bank routing and account numbers to the service provider).Instantaneous Transactions

The processing time for traditional ACH payments is typically between two and three business days; however, weekends and holidays can cause a delay in the transaction. That is much too slow, particularly for an electronic system, in this world of instant gratification that we live in today. Since 2016 marked the beginning of same-day ACH payments and given that functionality is currently being expanded, you should anticipate seeing faster payments in the near future.Questions That Are Typically Asked (FAQs)

What exactly is a debit using ACH?

A charge that is made against your checking or savings account is referred to as a debit. A debit card, in contrast to a credit card, deducts the amount directly from your bank account rather than from your available credit. A debit can be placed on your account in a number of different ways; an ACH debit is just one of those ways. An example of an ACH debit would be if the funds were taken out of your account through an electronic funds transfer (ACH).When during the day are ACH transactions processed and posted?

Transactions processed through ACH can be processed at nearly any time of the day, but transactions can only settle during business hours. Except for same-day payments, which have three additional settlement windows between 8:30 a.m. and 6:30 p.m. EST, all transactions are finalized and settled on weekday mornings at 8:30 a.m. Eastern Standard Time (EST).