The tax advantage that an ETF has over a mutual fund is one of its biggest advantages. To understand why ETFs are more tax-efficient than mutual funds, you must first grasp capital gains tax and how these two financial products are constructed. To put it another way, ETFs have a tax benefit over mutual funds since the underlying assets are traded less frequently, and individual investors can choose when to pay taxes by realizing gains. Still, perplexed? Continue reading to learn more about these themes.

Important Points to Remember

- Compared to mutual funds, exchange-traded funds have a number of tax advantages.

- Mutual funds trade assets more frequently than exchange-traded funds (ETFs), exposing mutual fund investors to additional capital gains taxes.

- ETF investors can also select when to sell their shares, allowing them to better manage capital gains taxes.

- ETF dividends, on the other hand, are not exempt from taxation and must be reported as soon as they are received.

Tax on Capital Gains

When you sell an asset for a profit, the government is entitled to a portion of the proceeds. The capital gains tax is a tax imposed on this profit. The government makes money if you make money. The Internal Revenue Service, on the other hand, does not regard all profits equally (IRS). The length of time you hold security determines your capital gains tax rate. If you sell a stock for a profit after holding it for a year or less, your profit will be taxed at the same rate as your income. Your gains are taxed at a special "long-term capital gains" rate if you own the stock for more than a year. The exact rate you'll pay on long-term capital gains will still be determined by your income tax band, although it'll almost definitely be lower than that.Mutual funds are more likely to trade their holdings.

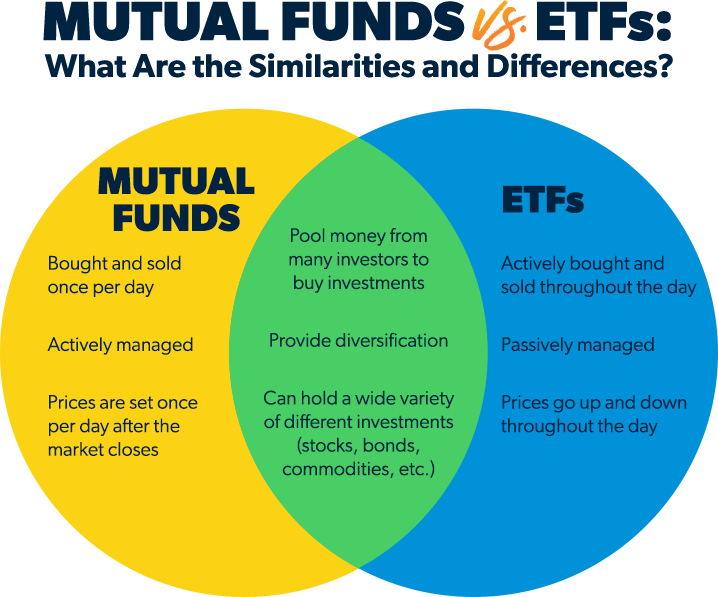

The vast majority of mutual funds are actively traded. When someone invests in the fund, the money is used to buy more shares by the fund manager. When someone sells some of their mutual fund shares, the fund manager must sell other holdings in order to reimburse the client for the shares they are selling. Capital gains taxes must be paid every time this happens when equities are sold for a profit. All of these small tax evasions might pile up over time. Investors also have no say in which shares are sold. Thus they have no say in whether capital gains are short-term or long-term. ETFs work in a very different way. Many popular index ETFs are handled passively. The underlying holdings of the ETF are evaluated less frequently, such as once a quarter. When those holdings are appraised, they are rebalanced to ensure that they continue to track the index. In many circumstances, rebalancing is more about deciding which stocks to acquire more of than it is about deciding which stocks to sell. ETF managers also do not have to acquire or sell stocks every time an investor buys or sells an ETF share. Because, unlike mutual funds, ETF shares are traded directly between investors, this is the case. Rather than going through the ETF manager, the seller trades the ETF shares directly with the buyer. With the support of institutional forces known as "approved participants," the ETF manager ensures that the share price represents the value of the underlying holdings. There's no need to trade underlying ETF holdings every time an investor sells a single share since authorized participants only trade in bulk amounts—typically 25,000 shares or more—so there's no need to trade underlying ETF holdings every time an investor sells a single share.The timing of ETF taxes is under the control of investors.

While the underlying shares of an ETF are traded less frequently, capital gains taxes still apply. However, there is a significant difference between ETFs and stocks in terms of the IRS: capital gains taxes are only paid by investors when the entire ETF is sold. 1 While you own ETF shares, you will never pay taxes on them. Capital gains taxes are usually distributed annually by mutual funds. The mutual fund manager will keep track of capital gains taxes, dividend payments, and capital gains profits throughout the year. Those odds and ends are distributed to investors at the end of the year in accordance with the number of mutual fund shares they own. Taxes may go unnoticed by mutual fund investors since they might be delivered at the same time as dividends, but they are there. Even if you didn't sell any mutual fund shares throughout the year, you'd be taxed. ETF investors can control when they pay capital gains taxes because they only pay them when they sell their shares individually. They can utilize timing methods to levy these taxes at a time when it is most advantageous. Their stock enjoys compound profits from tax deferral as they wait for the right time to impose the taxes.ETF investors will be subject to dividend taxes.

When it comes to taxes on ETF dividends, things are a little different. Rather, because ETFs do not benefit from special dividend tax treatment, things are the same as they are with other assets. Dividends will normally end up in your brokerage account as cash, whether you own a single stock, an index ETF, or a high-dividend ETF. Because you're getting paid in cash, you'll have to pay taxes on it. You won't gain any tax benefits if you receive a dividend from an ETF. While we're on the subject of dividend taxes, keep in mind that the IRS divides dividends into two categories: qualified and ordinary. Because they both receive preferential tax treatment, qualified dividends can be compared to long-term capital gains. When an investor holds an investment for a longer period of time, dividends become "qualified," just like long-term capital gains (more than 60 days). To be a qualified dividend, the dividend must be paid by a U.S. corporation in most situations, while some international companies pay qualifying dividends. An ETF investor can check to see if they've held the ETF for more than 60 days, but they can't check to see if the ETF manager has held the underlying stocks for that long. As a result, guaranteeing that dividends from ETFs are qualified is more difficult than ensuring payouts from individual stocks.Final Thoughts

In comparison to a mutual fund, an ETF offers two significant tax benefits. First, because of the high volume of trading activity, mutual funds are more likely to pay higher capital gains taxes. Second, an ETF's capital gain tax is deferred until the product is sold, whereas mutual fund investors must pay capital gains taxes while holding shares. Keep in mind that these benefits apply not only to ETFs but also to ETNs (exchange-traded notes). ETNs are similar to ETFs, but it's critical to understand all of the risks associated with any investment before making a trade.