Americans' complete Visa obligation keeps on climbing, coming to an expected $905 billion — a practically 8% increment from the earlier year — as per a NerdWallet examination. [1] Also, the typical family that is conveying charge card obligation has a surplus of $15,733. (By and large, the information examination found. 2017 family obligation concentrate on shows that few significant spending classifications have outperformed pay development over the last ten years; numerous Americans are putting clinical costs on Mastercards, and the typical obliged family is paying many dollars in Mastercard premium every year. This is the 2017 form of NerdWallet's yearly family obligation study. However, it's not all awful information: Household pay development is done being outperformed by the all-out average cost for many everyday items. Furthermore, as indicated by the aftereffects of another review, countless individuals with Mastercard obligations pin it on pointless spending, and that implies buyers can decide to chop their spending and pay down their equilibriums. Before Americans can start attempting to bring down their obligation, it means quite a bit to know the amount it is. This is the thing the normal obligated family owes, as well as all-out purchaser obligation, adjusts in the U.S., as per NerdWallet's examination: Sort of debt Total owed by normal U.S. family conveying this sort of debt Total obligation owed by U.S. customers Credit cards- $15,733 $905 billion Mortgages- $174,867 $8.74 trillion Auto loans- $27,807 $1.21 trillion Understudy loans- $46,831 $1.36 trillion Any sort of debt- $132,090 $12.96 trillion Obligation adjusts are current as of September 2017 The $905 billion in absolute Mastercard obligation determined by NerdWallet is lower than the $1 trillion usually referred to somewhere else in the media. That is because the $1 trillion gauges incorporate what's designated "set up overdraft plans" or overdraft credit extensions that don't be guaranteed to have a place with Mastercard clients. With these overdraft plans, buyers can pull out cash and make installments from the record with the credit line up to as far as possible. For past versions of our yearly family obligation study, as well as other Mastercard research, see our Credit Card Data page. Since NerdWallet's number spotlights Mastercard's obligation just, the $905 billion is a more exact gauge of how much obligation is exceptional. It's additionally vital to take note that this absolute incorporates the equilibriums of cardholders who cover off their cards consistently, as well as the individuals who convey obligation over time. To decide how much obligation Americans are conveying and the amount it's costing them in 2017, NerdWallet broke down information from a few sources, including the Federal Reserve Bank of New York and the U.S. Enumeration Bureau (see extra subtleties in the technique underneath). For this review, NerdWallet utilized a gauge of more than 126 million U.S. families given Census Bureau information. NerdWallet additionally authorized a review and gathered information, from more than 2,000 U.S. grown-ups in November 2017. In the study, Americans were gotten some information about their charge card installment propensities and how they strayed into the red. Figuring out how to put the cash toward taking care of obligations, particularly exorbitant premium obligations, is the most ideal way to liberate yourself from the tight clamp grasp obligation can have on your spending plan.

KIMBERLY PALMER, NERDWALLET'S CREDIT CARD EXPERT

Key discoveries Costs rise, and pay hasn't kept up. Throughout the last ten years, clinical expenses have expanded by 34% and food costs increased by 22%, which outperformed pay development (20%), NerdWallet's investigation found. [2] Medical care incurs significant damage. Up to 27 million U.S. grown-ups are putting clinical costs on charge cards, as indicated by NerdWallet's investigation, [3] costing them a normal of $471 in revenue for a year of cash-based clinical spending. That is more than $12 billion in aggregate. [4] Charge card obligation accompanies an expense. The typical family with a rotating Mastercard obligation pays $904 in interest every year. Pay becomes quicker than the cost for most everyday items Middle-yearly family pay has developed by 20% over the last ten years, while the average cost for many everyday items has expanded by 18%, NerdWallet's information investigation found. [6] However, huge costs in Americans' spending plans — clinical consideration, lodging, and food — have outperformed pay development. Four significant spending classes have expanded quicker than pay development beginning around 2007: clinical costs (34%), "other" costs (30%), food and refreshments (22%), and lodging (20%), as indicated by NerdWallet's investigation. [7] Furthermore, these costs are the absolute greatest for some Americans. Include the greater expense of residing in certain spots or persistent medical issues, and it tends to be significantly more earnestly for individuals to live without venturing into the red. With regards to Mastercard obligation, certain individuals believe it's the aftereffect of overspending, while others put it on the increasing cost for most everyday items for necessities. Our overview found that buyers amass Visa obligations for various reasons, including spending over their means, episodes of joblessness, and paying for the fundamentals that their pay doesn't cover. Around 2 out of 5 Americans who have at any point had Mastercard obligation (41%) announced that spending beyond what they could manage on superfluous buys added to them going into Visa obligation, the NerdWallet study found. A third (33%) said that spending on necessities their pay couldn't cover added to their charge card obligation adjusts. The increasing cost for many everyday items might be part of the way to a fault, especially in the spending classes, similar to medical services, that have expanded the most over the last ten years.What you can do

The expense of obligation incorporates the open doors you should do without taking care of it. In the NerdWallet overview, numerous Americans who have been in Visa obligation said that if they didn't have charge card obligation to pay off, they would set aside that cash for crises (57%), save it for a future objective (half) or potentially put the cash toward settling other obligation (33%). The speediest method for disposing of your obligation and begin making progress toward other monetary objectives is to slice costs to let loose money for bigger obligation installments. "Figuring out how to put the cash toward taking care of obligation, particularly exorbitant premium obligation, is the most ideal way to liberate yourself from the tight clamp grasp obligation can have on your financial plan," says Kimberly Palmer, NerdWallet's Visa master. "Making little strides, for example, ensuring reserve funds are in high return accounts, revising month to month bills, and utilizing a money-back Visa can let loose money that can be put toward obligation installments until they are settled upon off completely," she says. "Likewise, look around through your exchanges the most recent couple of months to see what things you can cut, for example, memberships, café dinners, or diversion costs."Clinical costs and the expense of interest

In the previous 10 years, clinical expenses have expanded by 34%, which is more than some other significant spending classes and essentially more than pay. [2] As indicated by a 2016-17 study by the Kaiser Family Foundation, which centers around the country's well-being approaches and clinical issues, 29% of Americans report issues covering hospital expenses, and 37% have expanded their charge card obligation to help take care of for doctor's visit expenses. In light of the number of grown-ups in the U.S. — just about 250 million as of July 2016 — NerdWallet's estimations found that almost 27 million Americans could be putting hospital expenses on Mastercards. [3] How about we think about expenses: The typical yearly cash-based clinical spending per capita in the U.S. was $1,054 starting around 2015, the latest information accessible from Peterson-Kaiser, an association between the Peterson Center on Healthcare and the Kaiser Family Foundation. Assuming this sum went on a charge card and the least installments were made every month, it would cost $471 in interest and require 70 months to pay off, as per NerdWallet's estimations. [4] Assuming each of the 27 million Americans who put doctor's visit expenses on a Mastercard paid this much interest, that would be more than $12 billion altogether. Charging doctor's visit expenses to Visas can appear to be a basic arrangement, however, it can prompt significantly greater cerebral pains not too far off.KIMBERLY PALMER, NERDWALLET'S CREDIT CARD EXPERT

What you can do

"Charging hospital expenses to Visas can appear to be a basic arrangement, however it can prompt significantly greater migraines not too far off," Palmer says. "That is because many charge cards have exorbitant loan fees, and that implies the sum owed can rapidly accelerate crazy. All things being equal, inquire as to whether you can orchestrate a without interest installment plan with them." One more cash-saving tip for medical services costs is by utilizing an adaptable spending course of action or a well-being bank account whenever presented by your boss. There you put cash to the side to pay for clinical costs. HSAs are accessible to individuals who utilize a high-deductible well-being plan, while FSAs don't have qualification prerequisites. Placing cash in one of these records implies you'll set aside charges and have money available for doctor's visit expenses.Expenses of rising Visa obligation

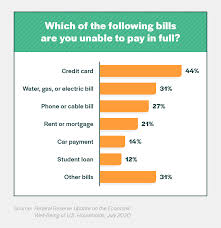

The Fed's latest Survey of Consumer Finances, delivered in October, showed an expansion in the quantity of U.S. families with Visa obligations: 43.9% in December 2016 contrasted and 38.1% in December 2013. The effect of a Visa obligation relies on how you handle it. There are two fundamental kinds of Mastercard clients, transactors, and guns. Transactors cover their Mastercard adjusts consistently and don't pay interest. Guns convey Mastercard obligation over time, paying interest on their normal day-to-day balance. In the NerdWallet overview, 61% of Americans who have at any point possessed a Mastercard said they have conveyed an equilibrium over time, either at present or beforehand. Visas regularly have twofold digit financing costs, in any event, for shoppers with astounding credit, so being a pistol can be costly. The typical U.S. family with a rotating Mastercard obligation conveyed a total of $6,081 as of June 2017. Accepting a loan cost of 14.87% — the ongoing normal — that total would cause $904 in interest each year, as indicated by NerdWallet's examination. [5]The cost of independent work

Being independently employed has its advantages — adaptable work hours, no chief, and the opportunity to deal with the things that energize you. In any case, it can likewise be expensive. Unpredictable pay and operational expense could assist with making sense of why independently employed people have more Visa obligations, which prompts higher loan fee costs. U.S. families driven by independently employed people pay $1,194 in Visa interest every year, contrasted and $843 for those whose employers are another person, as indicated by NerdWallet's investigation. Individuals who are resigned pay a yearly normal of $684 in Visa interest. [8]Expenses of homeownership

Certain individuals say leaseholders are wasting cash on a lease, however, obviously, they're discarding less on Visa revenue than their home-claiming companions. Tenants pay simply over a portion of what property holders pay in Mastercard interest every year, $537 versus $1,001, as per NerdWallet's investigation. [9] To lessen how much interest you're paying, think about making installments all the more habitually. KIMBERLY PALMER, NERDWALLET'S CREDIT CARD EXPERT Taken care of rate climbs and premium expenses The Fed meets on Dec. 12-13 to decide on whether to increment loan fees by a 0.25 rate point. This will affect anybody with a credit item — like a Visa or advance — with a variable financing cost. If the Fed increments rates, the normal yearly premium will ascend from $904 to $919, as per NerdWallet's investigation. [10] Albeit an increment of $15 every year, or a little more than a buck a month, doesn't seem like a lot, this could simply be the start. The Fed is supposed to keep on expanding rates in 2018 and 2019, so these numbers could keep on crawling up and add to customers' obligation loads. How might a Fed rate climb influence your Mastercard premium? Visa financing costs ordinarily ascend with the great rate, which is impacted by choices by the Federal Reserve. Our number cruncher allows you to reproduce the impact of a rate increment. Normal conveyed balance? $0 Loan cost (APR)? 0.00 Interest north of 1 YEAR $0.00 Interest north of 5 YEARS $0.00 If the Fed raised rates by ...? Pick Interest more than 1 YEAR $0.00 Interest more than 5 YEARS $0.00 What you can do As indicated by the NerdWallet review, of the Americans who have been in Visa obligation eventually, less than 1 of every 5 (18%) say they typically pay/settled upon their charge card balance completely every month. More Americans who have been in Visa obligation say they normally pay/paid however much cash they have leftover toward the month's end after all-important costs have been paid (26%) or a level sum they have assigned toward their obligation (26%), the study found. Under a quarter (23%) said they ordinarily pay/paid just the base sum due. It's wise to put more than the base installment toward your Mastercard obligation. In any case, it's ideal to cover the equilibrium every month to keep away from interest. If your equilibrium is too large, persistently make progress toward paying it down. "To diminish how much interest you're paying, consider making installments more oftentimes than once per month to hold your typical day-to-day balance down," Palmer says. "Another choice is to consider uniting Mastercard obligation onto a card with a 0% initial APR and no expense for balance moves. Then, you can chip away at taking care of the obligation before the starting time frame closes, which is regularly 12 to a year and a half."