Assume you've just turned 40 and have finally decided to educate yourself on the necessity of retirement planning. You may have even purchased a book or magazine on the subject. It says that you should have started saving for retirement in your twenties. You're way past that age and haven't even begun to put money aside for retirement. Even if you're running behind schedule, you do have options.

Important Points to Remember

- Increase the amount of money you save each year for retirement.

- Make a monetary target that is reasonable.

- Excessive danger should be avoided.

- Consider opening a Roth IRA.

- Check to see if you have enough insurance.

- Pay off debt with a high-interest rate.

- Don't go bankrupt to pay for your children's college education.

- Play a Catch-Up Game

Determine how much money you'll need to save.

You may convince yourself that you don't require a million bucks or desire a simple life. However, even a simple existence can necessitate having $1 million in the bank after retiring. During your retirement, most experts agree that you should remove no more than 3% to 4% of your retirement account each year. If you do the arithmetic, 3% of a million dollars equals $30,000, and 4% equals $40,000. In other words, if you want to retire with a $30,000 to $40,000 annual salary, you'll need a portfolio worth at least $1 million. That assumes you won't have a pension, rental properties, or other retirement income sources. It also doesn't include Social Security benefits.Don't take any more chances.

To compensate for the missed time, some people make the error of taking on greater investing risk. The potential profits are greater: Rather than 7%, there's a potential that your investments will grow by 10% or 12%. However, the chance of losing your money, or your principal, is significantly larger. Your risk level should always be proportional to your age. People in their 20s are more willing to tolerate larger losses since they have more time to recover. In their 40s, people may accept less risk, and in their 50s, even less. Accept no more risk in your portfolio. One of the following asset allocation algorithms might be worth considering:- Invest a percentage of your age less than 120 in stock funds, with the rest in bond funds. This is a high but manageable level of risk.

- Invest a portion of your money in stock funds equal to 110 percent of your age, with the rest in bond funds. This is associated with a lower level of risk.

- Invest a percentage of your money in bond funds equal to your age, with the rest in stock funds. This is a more conservative risk level.

Open a Roth IRA to Increase Your Savings

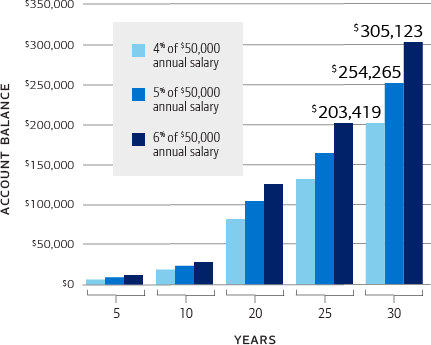

After maxing out your 401(k), start an IRA and contribute as much as possible. A 40-year-old eligible to contribute to a Roth IRA can significantly boost their retirement savings each year. Roth IRA contributions grow tax-free, and eligible withdrawals are also tax-free. You'll even avoid paying capital gains tax on your contributions' growth.Purchase Enough Insurance

Unforeseen circumstances bring on the majority of personal bankruptcies. Reduce your risk by purchasing enough health, disability, and automobile insurance. If you have dependents, consider term life insurance for the period during which they will be financially reliant on you. According to many financial experts, whole life insurance isn't always the best decision, especially if you're starting coverage in your 50s. Seek out planners who owe you a "fiduciary obligation" as a customer. According to many financial experts, whole life insurance isn't always the best decision, especially if you're starting coverage in your 50s.Debt Reduction

Credit card debt, vehicle loans, and other high-interest or non-mortgage debt should be paid off as soon as possible. On the other hand, paying down debt should not come at the expense of your financial goals. Having a financial plan to pay off debt and put money aside for retirement is critical. Consider whether you should make additional mortgage payments. If you're in the early stages of your mortgage and most of your payment goes toward interest, paying down part of the principal would be a good idea. If, on the other hand, you're nearing the end of your mortgage and your payments are mostly going toward the principal, you could be better off putting that money into retirement.Priority is given to you and your spouse.

Don't squander your retirement money to pay for your children's college education. Your children have more choices and possibilities than you do. You may or may not be able to take out a loan against your 401(k) account balance. Your children, in any event, have their entire life ahead of them. They can begin saving for retirement as early as their twenties and thirties. You can't go back in time and reclaim those decades of retirement savings if you're in your 40s. As a result, the finest gift you can give your children is your financial retirement.Most Commonly Asked Questions

- What is the best way to begin saving for retirement?

- When should the average person begin putting money down for retirement?