Bottom line: The simplicity of Ladder's tech-forward approach to life assurance could also be appealing, but the shortage of optional riders may deter customers looking to customize coverage.

LADDER life assurance

We gave it a 3.5-star rating. Sells term life assurance nationwide with a web application. Many applicants can qualify without taking a checkup. The Ladder is an insurance startup offering term life assurance to people ages 20 to 60. the corporate was founded in 2015 and has since expanded to all or any 50 states and Washington, D.C. In 2020, it announced an expansion to its partnership with private nondepository financial institution SoFi and legal instrument platform NetLaw to permit SoFi members to make wills free of charge. Why you'll trust Us: Our writers and editors follow strict editorial guidelines to make sure the content on our site is accurate and fair. You'll make financial decisions confidently and choose the products that employment best for you. Here may be a list of our partners, and here's how we make money.Ladder life assurance

Ladder earned 3.5 stars out of 5 for overall performance. The scoring formula takes into consideration consumer experience, complaint data from the National Association of Insurance Commissioners, and financial strength ratings. Our editorial team determines our ratings.Ladder life insurance Positives and Negatives

| Positives | Negatives |

| Applying and managing your account online are simple. | Some Ladder policies are issued by a firm that has received significantly more consumer complaints to state authorities than one would expect from a firm of its size. |

| Most applicants won't need a medical exam. | No riders to add to your policy. |

| Coverage limits up to $8 million. |

Ladder life assurance policies

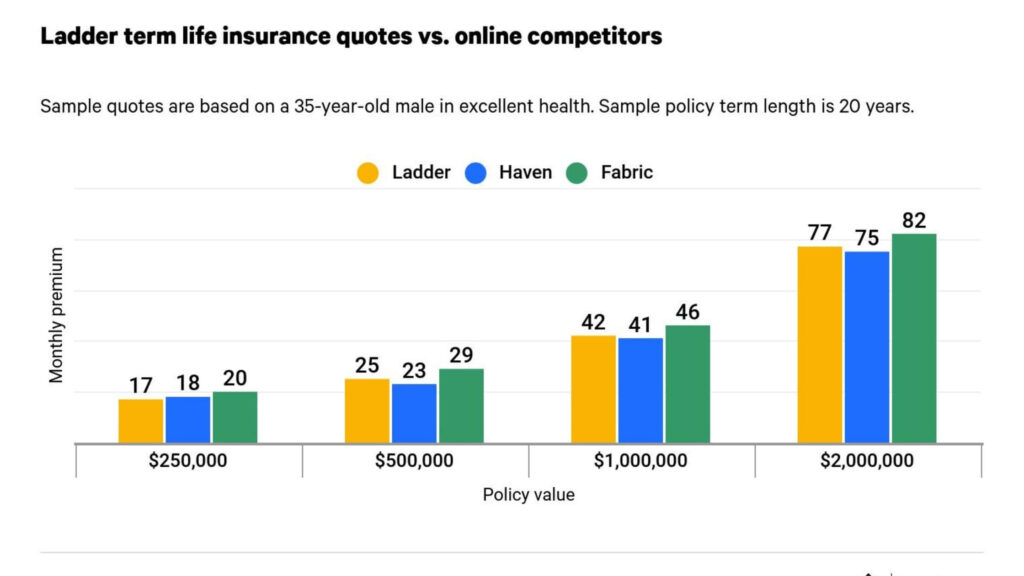

Ladder emphasizes a streamlined experience by selling and managing policies online without the use of agents and providing quick coverage determinations, allowing some consumers to be covered minutes after applying. Depending on your age, Ladder offers plans up to $8 million with terms of 10, 15, 20, 25, and 30 years. It's possible that your age and the length of your chosen term do not equal 70. Applications for coverage of $3 million or less are often completed online, without the necessity for a checkup. There are not any riders available to feature to a policy. Ladder lets customers decrease or apply to extend their coverage amount online when their needs change. Ladder policies are issued by Allianz life assurance Company of latest York, Fidelity Security life assurance Company, and Allianz life assurance Company of North America.Ladder customer complaints and satisfaction

Over three years, Allianz Life has drawn fewer than the expected number of complaints to state regulators. Fidelity Security Life has drawn much more complaints than expected for companies of its size, consistent with our analysis of knowledge from the National Association of Insurance Commissioners.More about Ladder life assurance

Ladder's website is cleanly designed and mobile-friendly, with a web quote process that provides you with a fast cost estimate in minutes. (For a final quote, you'll have to provide more in-depth information.) The site offers a guide to life assurance basics also as a calculator to assist you in working out what proportion of coverage you would like. The Ladder mobile app is liberal to download. You'll apply for coverage directly through the app and reduce or apply to extend coverage at any time. The Ladder doesn't sell any products beyond term life assurance.Life insurance buying guide

Before you begin comparing companies:- Choose the sort of life assurance you would like, like the term or whole life.

- Calculate the proportion of life assurance you would like and how long you would like the coverage to last.

- Decide which life assurance riders, if any, you would like the policy to incorporate. Ensure the insurers you're considering offer the coverage you're trying to find.

Life insurance rating methodology

Our life assurance ratings are supported by consumer experience, complaint index scores from the National Association of Insurance Commissioners for individual life assurance, and weighted averages of financial strength ratings, which indicate a company's ability to pay future claims. Within the buyer experience category, we consider simple communication and website transparency, which looks at the depth of policy details available online. To compute each insurer's rating, we converted the data to a curved 5-point scale. These ratings are a guide, but we encourage you to buy around and compare several insurance quotes to seek out the simplest rate for you. We don't receive compensation for any reviews. Read our editorial guidelines.Insurer complaints methodology

We examined complaints received by state insurance regulators and reported to the National Association of Insurance Commissioners in 2018-2020. To assess how insurers compare to at least one another, the NAIC calculates a complaint index annually for every subsidiary, measuring its share of total complaints relative to its size or share of total premiums within the industry. Auto, house (including renters and condos), and life insurance ratios are all calculated independently. To gauge a company's complaint history, we calculated an identical index for every insurer, weighted by market shares of every subsidiary, over a three-year period.